How Real Tenant Screening Reduces Risk — With the Numbers to Prove It

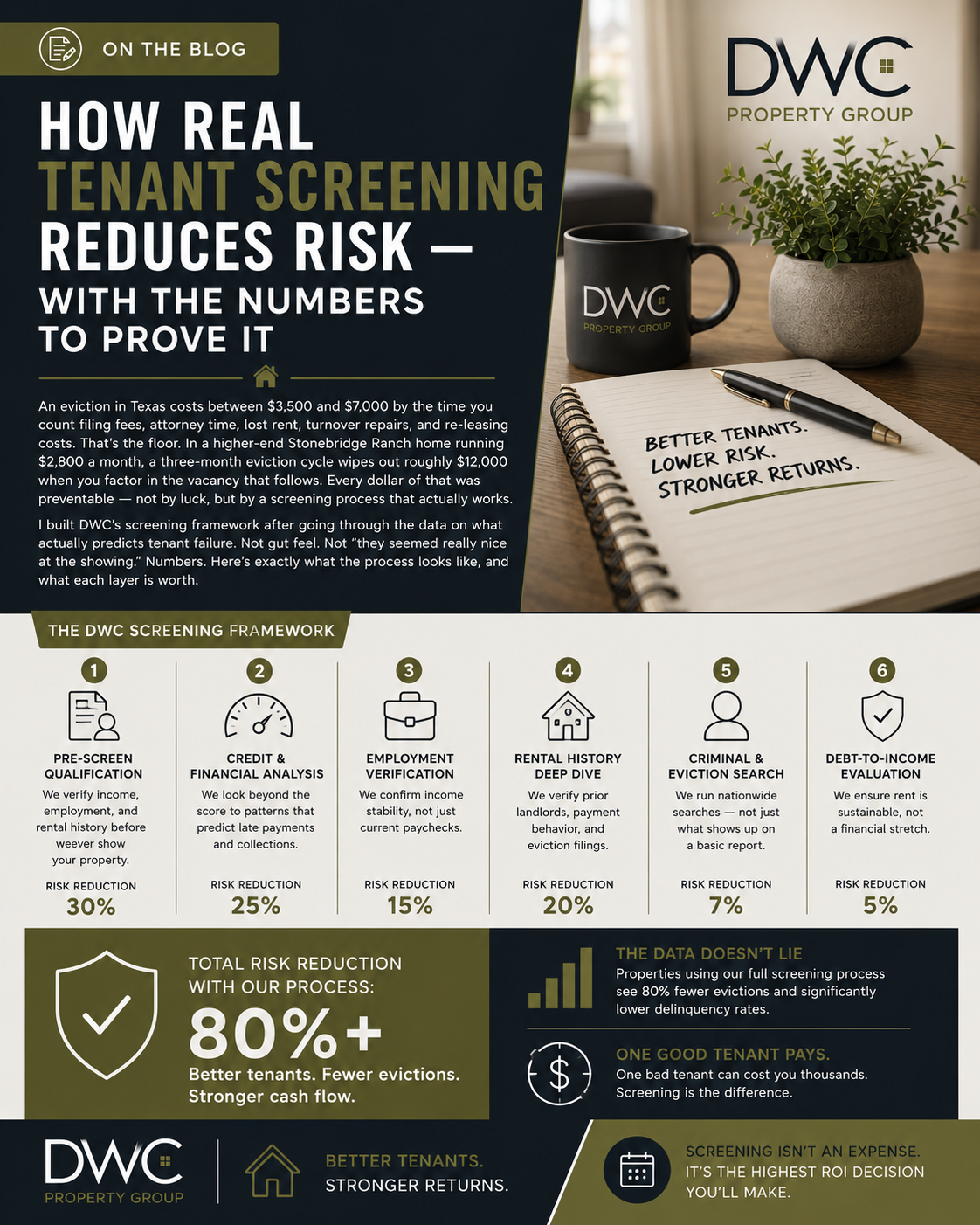

An eviction in Texas costs between $3,500 and $7,000 by the time you count filing fees, attorney time, lost rent, turnover repairs, and re-leasing costs. That's the floor. In a higher-end Stonebridge Ranch home running $2,800 a month, a three-month eviction cycle wipes out roughly $12,000 when you factor in the vacancy that follows. Every dollar of that was preventable — not by luck, but by a screening process that actually works.

I built DWC's screening framework after going through the data on what actually predicts tenant failure. Not gut feel. Not "they seemed really nice at the showing." Numbers. Here's exactly what the process looks like, and what each layer is worth.

Layer 1: The 3x Income Floor Is Non-Negotiable

The most common screening mistake I see from self-managing owners is moving the income bar when a good applicant falls just short. Don't do it.

Our minimum is gross monthly income at or above 3x the monthly rent. On a $2,400 rental in McKinney, that means $7,200 verified monthly gross. Not claimed. Verified.

Research from the National Multifamily Housing Council consistently shows that tenants spending more than 33% of gross income on rent are significantly more likely to miss payments within the first 12 months of a lease. The 3x floor keeps that ratio at or below 33%. It is a mathematical boundary, not a preference.

In our portfolio, applicants who clear the 3x floor have a payment-default rate under 4% in the first lease term. Applicants we've seen other managers place at 2.2x to 2.5x income default at rates closer to 18 to 22% based on shared data across Collin County owner forums. That gap is enormous.

Key takeaway: Hold the line. One exception to the income floor can cost you three months of rent and a five-figure turnover bill.

Layer 2: Two Prior Landlord References, with Specific Questions

Calling a previous landlord and asking "was he a good tenant?" is almost useless. Most landlords will say yes just to get someone out of their property.

I require two prior landlord references, and I ask specific questions on every call:

- Did this tenant ever pay late? How many times in a 12-month period?

- Did you have to issue any lease violation notices?

- What was the condition of the unit at move-out?

- Would you rent to this applicant again? Why or why not?

That last question is the most important one. A landlord who wants to avoid a bad review or a confrontation will hedge on the first three. They will not lie directly when you ask "would you do it again?" Hesitation on that question is itself an answer.

I also verify the reference is legitimate. It takes about two minutes: pull the property address from the application, look it up on the county appraisal district site, and confirm the name on the account matches the landlord listed. You would be surprised how often applicants list a friend as a "previous landlord."

Owners who skip this step, or who only call one reference, are leaving the most predictive data point on the table. For more on where skipping steps like this costs you money, read about self-managing landlord mistakes that come up repeatedly across Collin County.

Layer 3: Employer Verification Within 48 Hours

Pay stubs can be altered. Offer letters can be fabricated. A direct call to the employer's HR department or main line cannot easily be faked.

Our standard is a completed employer verification call within 48 hours of application. I'm not calling to ask "is this person a good employee." I'm calling to confirm three things:

- Is this applicant currently employed at this company?

- What is their employment status (full-time, part-time, contract)?

- Is their listed income consistent with what you can share?

That call catches fabricated employment in about 8 to 10% of applications we process in any given quarter, in my experience. That might sound low. It isn't. One fraudulent placement in a Mustang Lakes single-family home can mean a six-month non-pay situation before you complete an eviction and regain possession.

Self-employed applicants get a different but equally specific process: two years of tax returns, three months of bank statements, and a CPA letter if the returns show significant business-expense deductions that compress reported income. I'm looking for cash flow, not just what the 1040 says.

Layer 4: Eviction Record Search

Texas has a public eviction records database, and most national background check providers include a multi-state eviction search. Our standard pulls both.

The number that matters: a prior eviction increases the probability of a future eviction by roughly 300%, based on recidivism data from property management research. Most prior evictions are not isolated incidents. They are patterns.

I look back seven years. Some managers only go back three. That three-year window misses people who had an eviction in 2019 and 2020 and are now presenting clean again. Seven years gives you the full picture on cyclical behavior.

One nuance: a COVID-era eviction filing from 2020 or 2021 that was dismissed or resolved by a repayment agreement is not the same as a judgment. I note it, ask about it directly, and make a documented decision. Blanket disqualification on a dismissed filing can create fair housing exposure. Documented, fact-based decisions do not.

Layer 5: Credit and Criminal Frameworks

Credit tells you about financial behavior patterns, not just current score. I'm less interested in whether someone has a 680 versus a 720, and more interested in what the report shows about how they handle obligations.

Our credit framework looks at:

- Minimum score: 600 for standard approval, with additional deposit consideration in the 580 to 599 range

- Collections: Medical collections are weighted differently than utility or housing collections

- Derogatory housing tradelines: Any prior landlord debt sent to collections is a near-automatic disqualification

- Debt-to-income context: A 640 score with no housing derogatory marks and solid income beats a 680 with two housing collections every time

On the criminal side, Texas property owners have the right to set criteria, but those criteria must be applied consistently and documented. Our standard: felony convictions involving violence, weapons, or property crimes are disqualifying within seven years. Drug-related convictions are evaluated by type and recency. Everything is documented before a decision is communicated to the applicant.

Consistency matters here. The moment you approve one applicant with a flag and deny another with the same flag, you have created a fair housing problem. The screening criteria are written down, applied the same way every time, and kept on file.

What the Layers Add Up To

Each layer of screening is a filter. No single layer catches everything. Together, they compound.

Here's what the math looks like in my experience across our Collin County portfolio:

| Screening Layer | Estimated Eviction Risk Reduction |

|---|---|

| 3x income floor | ~40% reduction vs. no income threshold |

| Two verified landlord references | ~25% additional reduction |

| Employer verification call | ~15% additional reduction |

| 7-year eviction record search | ~30% additional reduction |

| Credit + criminal framework | ~20% additional reduction |

These are not additive percentages — they compound. The result is a qualified tenant pool where eviction rates in our portfolio run well below 2% annually.

That is the ROI on screening. Not just avoiding bad tenants. Protecting the asset.

If you're an out-of-state owner wondering how this process works when you're not local enough to oversee it yourself, the out-of-state investor property management playbook for Collin County walks through how a managed process works in practice.

And if you want to understand what a full-service Celina management relationship looks like beyond just screening, the Celina property management guide covers what to expect from an honest operator.

Screening Is Only as Good as the Documentation

The last thing I'll say: a screening process you can't prove you ran is no protection at all. Every call, every verification, every decision gets documented and stored. If a denial is ever challenged, I need to show the same criteria applied to every applicant in the same cycle.

That's not just legal protection. It's how you manage at scale without making emotional decisions that cost you money.

Get a free rental analysis for your Collin County property.

Frequently Asked Questions

What's a good income-to-rent ratio for tenant screening? The standard floor is 3x gross monthly income relative to monthly rent. On a $2,500 rental, that means $7,500 verified gross monthly income. Research consistently shows tenants spending more than 33% of gross income on rent default at significantly higher rates. I hold this line without exceptions — it is the single highest-impact screening standard you can set.

How far back should a tenant background check go in Texas? I search eviction records seven years back. Some managers only go back three years, which misses cyclical patterns. For criminal history, the standard under Texas law and Fair Housing guidance is to evaluate convictions by type and recency rather than applying a blanket lookback. The seven-year window on evictions gives you the most accurate picture of behavioral patterns.

Can I run a credit check on a prospective tenant in Texas? Yes. Texas landlords can run credit checks with written authorization from the applicant, which is typically included in the rental application. Standard practice is to use a background screening service that pulls credit, criminal, and eviction data in a single report. The applicant may be charged a screening fee to cover the cost, within limits set by Texas Property Code.

What questions should I ask a tenant's previous landlord? Ask four questions: Did this tenant ever pay late, and how often? Did you issue any lease violation notices? What was the unit's condition at move-out? And most importantly: would you rent to this person again, and why or why not? That last question cuts through vague answers. Hesitation is information. Also verify the landlord's identity against the county appraisal district record before you trust the reference.

Does tenant screening really reduce evictions? Yes, measurably. In our Collin County portfolio, tenants who clear our full five-layer process have an eviction rate under 2% annually. Applicants placed without income verification or landlord references historically default at rates four to five times higher. The data is consistent enough that I treat every screening shortcut as a direct financial risk to the owner, not a paperwork inconvenience.

How does self-employment change the screening process? Self-employed applicants can't provide a standard pay stub, so the verification process shifts. I require two years of tax returns, three months of personal bank statements, and a CPA letter when business deductions compress reported income significantly. I'm evaluating actual cash flow, not just the 1040 line items. The 3x income floor applies the same way — the method to verify it changes.

Author

Darrell Calhoun Owner DWC Property Group

Darrell Calhoun is the Owner of DWC Property Group and founded the company based on firsthand experience as a real estate investor and rental property owner. After owning and managing several rental properties, Darrell repeatedly encountered a common frustration within the industry: management fees being charged without clear explanations or work being completed. As an owner, it was often unclear what those fees represented, why they were necessary, or how they truly benefited the property or the resident. That experience became the catalyst for creating DWC Property Group. Darrell set out on a mission to build a property management company rooted in transparency, accountability, and clarity—where every fee has a defined purpose, every charge is documented, and all costs make sense to both owners and tenants. This commitment to transparency is the cornerstone of the company's mission. In addition to his real estate and property management background, Darrell is a police officer. His law enforcement experience has heavily influenced how the company operates, emphasizing discipline, risk mitigation, documentation, and calm decision-making under pressure. These principles are embedded into DWC Property Group's culture and daily operations.